Global alcohol consumption declined by 1.6% to 27.6 billion nine-litre cases of alcohol in 2018, according to IWSR, but it is expected to steadily rebound to to 28.5 billionn cases in 2023, according to IWSR.

In terms of retail value, the global market for beverage alcohol in 2018 was just over US$1trillion, a number which the IWSR expects to grow 7% by 2023 as consumers continue to trade up to higher-quality products.

In both wine and beer sectors, as the report noted that waned demand from China dragged down the two categories’ consumption.

Wine

Wine, which had posted strong global growth in 2017, lost -1.6% in volume in 2018 as wine consumption declined in major markets such as China, Italy, France, Germany and Spain (the US market was flat). However, though consumers are drinking less wine, they’re increasingly drinking better – pushing wine value to increase.

Globally, the retail value of wine is projected at US$224.5bn by 2023, up from US$215.8bn in 2018. The one brightspot in wine volume is the sparkling wine category, which is expected to show a five-year CAGR of 1.17% 2018-2023, driven in large part by prosecco.

Gin

The largest gain in global beverage alcohol consumption in 2018 was in the gin category, which posted total growth of 8.3% versus 2017. Pink gin was a key growth driver, helping the category sell more than 72m ninelitre cases globally last year. In the UK alone, gin was up 32.5% in 2018, and the Philippines (the world’s largest gin market) posted growth of 8%, fueled by a booming cocktail scene and premiumisation of the market. By 2023, the gin category is expected to reach 88.4m cases globally, with particular strong growth in key markets such as the UK, Philippines, South Africa, Brazil, Uganda, Germany, Australia, Italy, Canada and France.

Beer

Beer Continued to Lose Volume in 2018, but is Expected to Rebound Global beer declined -2.2% in 2018, impacted greatly from volume decreases in China (-13%). Other large markets such as the US and Brazil also fell (-1.6% and -2.3%, respectively), while Mexico and Germany saw growth (6.6% and 1%, respectively). The future outlook for beer, however, paints a more positive picture, as the

category is expected to show a slight increase in 2019 and post a 0.7% CAGR 2018-2023.

Whisky and Agave-Based Spirits

Spurred by innovation in whisky cocktails and highballs, the global whisky category increased by 7% last year,driven in large part by a strong Indian economy (whisky grew by 10.5% in India, as consumers continue to trade up in the category). The US and Japan posted 5% and 8% growth, respectively. The IWSR forecasts whisky to grow by 5.7% CAGR from 2018 to 2023, to almost 581m nine-litre cases. Also, continued interest in tequila and mezcal (especially in the US), and innovation in more premium variants and cocktails, drove the agavebased spirits category to 5.5% global growth in 2018 – and is expected to post 4% growth over the next five years (2018-2023 CAGR).

Low- and No-Alcohol Products

Low- and no-alcohol brands are showing significant growth in key markets as consumers increasingly seek better-for-you products, and explore ways to reduce their alcohol intake. Growth of no-alcohol beer is expected at 8.8%, and low-alcohol beer at 2.8%. No-alcohol still wine is forecasted at 13.5%, and low-alcohol still wine at 5.6%. Growth of no-alcohol mixed drinks is predicted at 8.6%. (Above figures are all CAGR 2018-2023.)

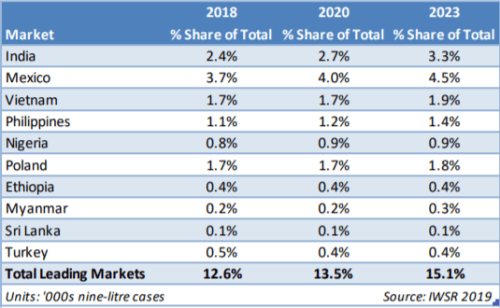

Top Ten Performing Global Markets, 2018-2023

A look at the world’s fastest-growing beverage alcohol markets shows an emergence across a variety of developing countries. A combination of growing legal-drinking-age populations and healthy economies is driving some of this growth, which is expected to continue over the next five years.

Discover more from Vino Joy News

Subscribe to get the latest posts sent to your email.